Article Published in Forbes

The One Question You Should Be Asking In Retirement

Yogi Berra once said, “When you come to a fork in the road, take it.” As a retiree or pre-retiree, you've worked diligently and built your life savings. Now's the time to ask the No. 1 question every retiree should be asking:

Everyone has unique wants, needs, and values, and the amount of risk each person is willing to take differs as well. Getty Images

What do you want out of retirement?

To help you answer this question, here's a list of more specific questions to help shape your retirement picture:

- Do you want to continue to grow your nest egg, build more wealth, and leave a legacy?

- Does risk bother you, or are you willing to keep your money in the market?

- Do you have a written financial plan?

- Are your health care costs covered?

- Do you have enough money and know that you won't run out of money in retirement?

- Do you want tax-free money in retirement, and how can you get that?

- Do you believe that taxes will go up in the future?

- Do you think Social Security is safe? Will the benefits be lower or higher?

- Are you concerned about market volatility and sequence of returns?

- Where is inflation headed — higher or lower?

Each individual and couple has unique wants, needs, and values, and the amount of risk each person is willing to take differs as well. Below, I'll break down what I believe to be the three most important steps toward planning for and building the lifestyle you want in retirement.

A Needs-Based Foundation

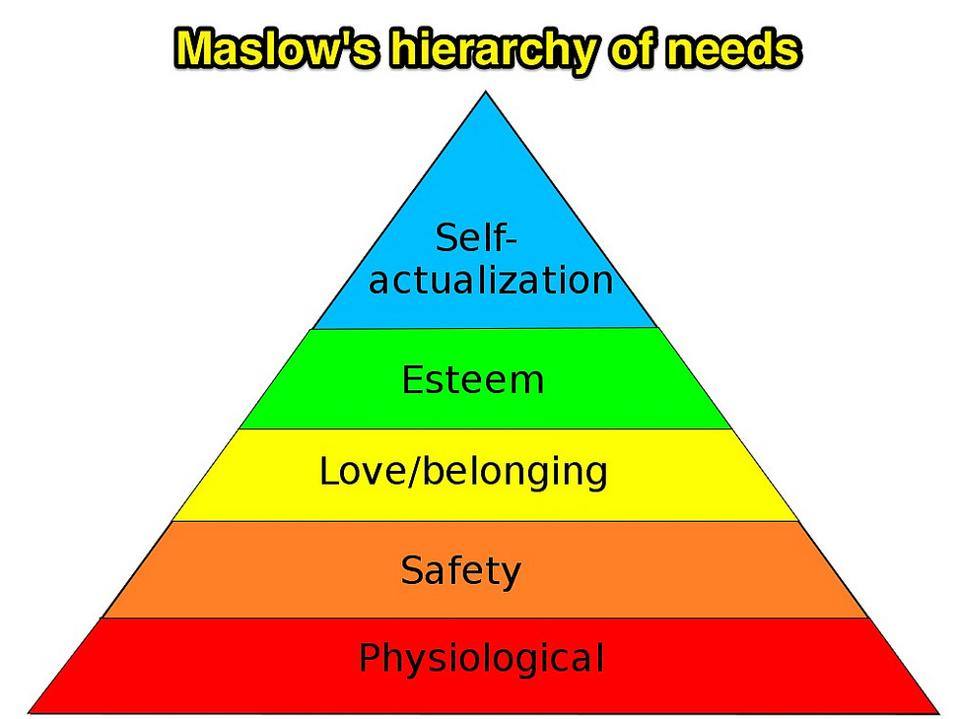

Wikipedia: http://en.wikipedia.org/wiki/Maslow%27s_hierarchy_of_needs

The above is Maslow's hierarchy of needs. While Maslow intended it for basic human needs, I believe sound financial planning should follow it, too.

At the base are our physiological and safety needs. Life savings provide added safety, food, clothing, and shelter. This part of your retirement plan should be rock solid. You have saved for retirement, and this portion should be conservative with very little risk involved. Why would you take unnecessary risk with this part of your life savings?

The next part of your retirement plan is love/belonging, is the fun part of retirement. Once you have the added safety to your plan, develop the time to have fun with your spouse/significant other and family — maybe it's traveling or going to grandkids' soccer games.

Esteem and self-actualization are the legacy planning parts of your portfolio. What, if anything, do you want to leave to your family or a charity?

Risk Management

I grew up as a farm kid — I was driving a tractor at age 12 and helping my dad with the wheat harvest each year. I learned some powerful lessons at an early age that served me well.

I remember a very hot July day; we were just starting the yearly wheat harvest. A storm cloud was welling up on the horizon, and it soon was over our farm. In about five minutes, a hail storm wiped out our entire crop; a year's worth of work and income down the drain. I felt so bad for my dad and watched how he handled that adversity. He had some crop insurance, but it really wasn't enough.

That day taught me the importance of mitigating risk in life.

At the age of 42, I had an injury that ended my dentistry career. You never think it can happen to you, and my practice was at its peak. I was in my kitchen and got a bottle of apple cider out of the fridge. The kids were out trick-or-treating on Halloween night. I stepped over to the sink, and the bottle exploded in my right hand, severing the nerves, arteries, veins, and tendons in my thumb and index finger. Despite several surgeries and months of physical therapy, the nerves just didn't respond. Everything my wife and I worked for was ruined.

That experience left me with a dilemma: What am I going to do now? In retirement, you should be asking what level of risk you're willing to take with your savings. In the event of a market downturn, do you have a plan in place to mitigate risk and provide added protection?

An Active Retirement Plan

It's always been my mission to help people; now, I perform an exam, diagnosis, and comprehensive treatment plan for someone's life and retirement instead of their mouth. Smart, active management of retirement planning is essential.

I believe each person preparing for retirement should have a comprehensive financial analysis (exam) done of their portfolio. This risk analysis will evaluate how much risk you're willing to take as you approach retirement. Then, by sitting down and evaluating your goals and values for retirement, a complete financial plan (diagnosis) and retirement income plan (treatment plan) will be developed.

Your retirement income plan should reflect your risk tolerance — your goals and desires to give you the lifestyle you want in retirement. I believe a sound financial plan is the foundation for investor success. Keep in mind that everyone's risk tolerance is different — some will want to keep their nest egg in the market, while others will strive to mitigate risk through an actively managed portfolio alongside other concepts of tax-free income planning or annuities to help secure some future income.

Using active investment management processes designed to maximize each client's returns while minimizing risk is extremely important for long-term success. I firmly believe investment returns should be measured for consistency with the goal of protection from market losses.

Retirement income planning is one more step in developing your plan. We fully understand that creating a more stable income for retirement requires a blend of current income and future growth. It's important to consider where this income will come from.

By taking into account your personal retirement income needs, the amount of risk you're willing to take, and the development of a retirement plan, you can start moving toward the retirement lifestyle you want.

Investment advisory services offered through Retirement Wealth Advisors Inc. (RWA), a Registered Investment Advisor. Charlie Dingman and RWA are not affiliated. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision. DT![]() 534201-0619

534201-0619

"Through Financial Planning You Can Achieve Financial Independence"

Please Call Anytime: (406) 624-6465

Click Here to Send a Message